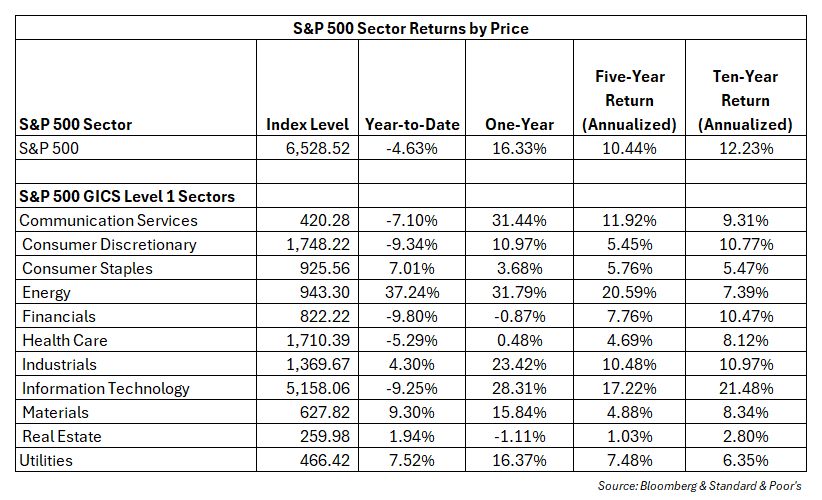

The first quarter saw the S&P 500 fall 9.79% peak-to-trough on an intraday basis. The S&P 500 touched 7,002.28 on January 28th and got as low as 6316.91 on March 30th before closing at 6,528.52, down 4.63% for the quarter.

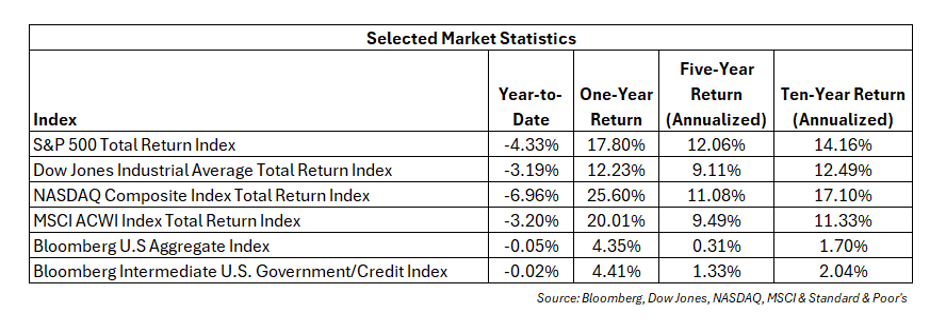

International indices outperformed the S&P 500 but still finished a touch lower. The MSCI Emerging Market Index fell a modest 0.51%, while the MSCI EAFE Index fell 1.87% (source: Bloomberg), Both indices outperformed the S&P 500. International equity outperformance was impressive given the 1.67% rise in the dollar.

The reasons behind the rise in the dollar are debatable. We feel one of the primary reasons is that the United States is a net exporter of energy, and this helped the dollar. Meanwhile, gold’s place as a safe haven came into question. Gold rose 28.68% to $5,586.20 on January 29th, before ending the quarter at 4,691.60, up 8.07% (source: Bloomberg). While this was an impressive return, it did not hold up during much of the equity selloff. It experienced a peak-to-trough first quarter decline of 26.60%.

The first quarter decline in the S&P 500 was led by weakness in hyperscalers, software stocks, and selected financials. A market that had embraced AI started to worry that AI disruption would hurt incumbent tech companies in addition to some of the debtholders.

Treasury yields rose modestly in the first quarter. In addition, corporate credit spreads widened modestly (source: Bloomberg). Accordingly, fixed income generated muted returns. The Bloomberg U.S. Aggregate Index finished the quarter close to flat, falling 0.05%. Despite flat returns, fixed income did help stabilize client portfolios.

Higher Oil Prices Raise Inflation Risks

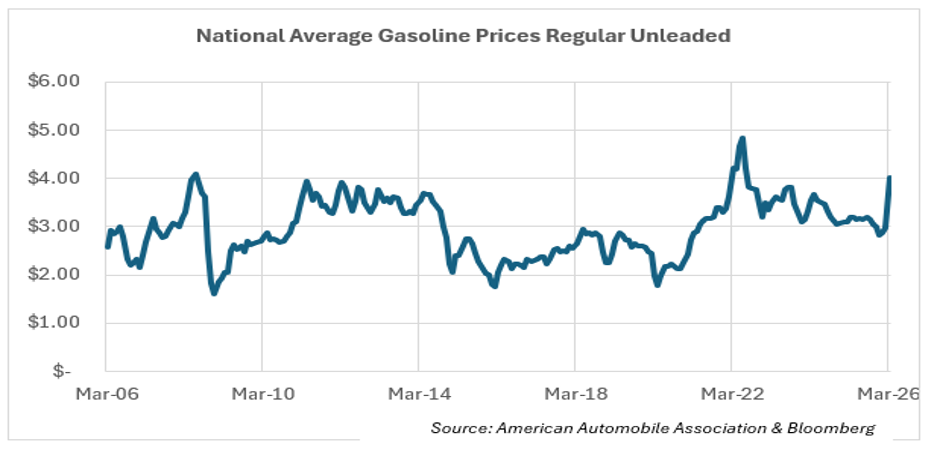

The US-Israeli war with Iran caused oil prices to spike from the 2025 year-end price. West Texas crude prices ended the quarter up 76.56% (source: Bloomberg). Energy spikes usually raise inflation concerns, and the current environment is no exception.

No one knows how long the current war will last. A sustained fight would likely leave oil prices higher. Even if there is no more damage to global energy infrastructure and the Strait of Hormuz fully reopens, the risks are high, and energy prices will likely remain elevated until the war ends. The damage to some energy facilities and the inability of U.S. frackers to immediately add capacity increases the likelihood prices will remain higher for longer after the initial price spike fades (Source: Morenne, B (2026.03.04), WSJ.COM).

This war has already led to rising gasoline prices (see chart). This should dampen real consumer spending but is unlikely to cause an economic contraction. Prices at the pump were higher in 2022 after Russia’s invasion of Ukraine, yet the economy avoided a recession.

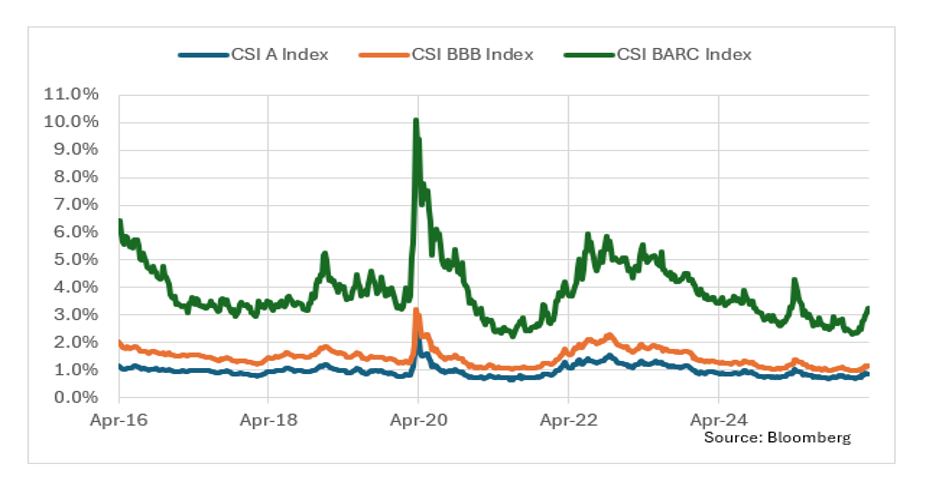

Treasury Yields and Credit Spreads Rise

Treasury yields increased across the curve in the first quarter of 2026. The Ten-Year Treasury rate rose 0.15% and ended the quarter at 4.32%. Arguably more importantly, the Two-Year Treasury jumped 0.32% and finished the quarter at 3.79%. Many market participants feel that the Two-Year Treasury leads the Fed Funds rate. Accordingly, the market is unsure if the Federal Reserve will lower rates at all this year and for a brief period thought a rate hike was more likely (source: Bloomberg). At the beginning of the year, the assumption was that the next move would be to lower rates (source: Bloomberg). This was at least temporarily a significant shift in monetary expectations.

Corporate credit spreads widened modestly in the first quarter of 2026 (see chart). Investment grade and high-yield corporate credit moved from extremely low readings to levels that are still below the ten-year average despite the recent runup. Investors frequently focus on equity markets, but bond markets are usually a better indicator of financial stability. The current levels are not worrisome but need to be monitored. The reasons for the increase in corporate spreads include the rise in Treasury yields, inflation worries and economic uncertainty, rising supply from large-cap tech to fund the AI buildout and worries about the private credit market. High-yield spreads increased more than investment-grade corporates, but they all remain below their ten-year averages.

The supply of private credit has grown rapidly over the last decade or so (Source: Ip, G (2026.03.28), WSJ.COM). More recently, these direct loans to private companies have seen rapid adoption by retail investors. Institutional investors primarily purchased them in funds where the ability to receive a return of capital was delayed for years. To gain access to retail channels, these loans were bought by credit interval funds, among other vehicles. Credit interval funds usually allow five percent of investor capital to be returned once a quarter. Unfortunately, investors in many private credit funds asked for their money back and this led several funds to cap the return of capital at five percent.

A couple of bankruptcies, concerns about software companies’ ability to repay their private credit debts, along with market volatility contributed to investors asking for their money back. While Continuity believes private credit was sold too much too fast to retail investors, the size of the markets and the five percent quarterly withdrawal restriction limit the economic damage. Continuity does not believe that problems lurking in private credit will lead to contagion. However, we will continue to monitor private credit conditions, and like any loan category, the trend bears watching.

Equities Decline in the First Quarter

The S&P 500 dropped 4.63% in the first quarter, led by the decline in financial stocks, hyperscalers, and software companies. There were a variety of factors that contributed to the decline in the financial services sector. The concerns in private credit markets led to large selloffs in private credit companies while credit card companies fell due to economic concerns. Private credit is one of the main market concerns at present, but we would be more concerned about it if bank stocks were doing worse. Most bank stocks have fallen, but not too much. In our opinion, this increases the likelihood that the losses in private credit are manageable.

Technology stocks also underperformed the broad market, but the pattern was not uniform. Hardware stocks outperformed software and internet companies. Many software companies experienced large declines as investors worried if their future cash flows would decline due to AI models. Hyperscalers fell due to AI concerns and the high debt levels needed for the data center buildout. Meanwhile, companies that make or manufacture semiconductors, storage and other equipment did extremely well.

Energy, materials, and utilities were the best-performing sectors. Middle East turmoil and the capex needs of data centers contributed to rising demand for hard assets. Whether this trend continues remains to be seen. The buildout is likely to continue, but now valuations in some of the recent mega-cap tech winners have declined materially.

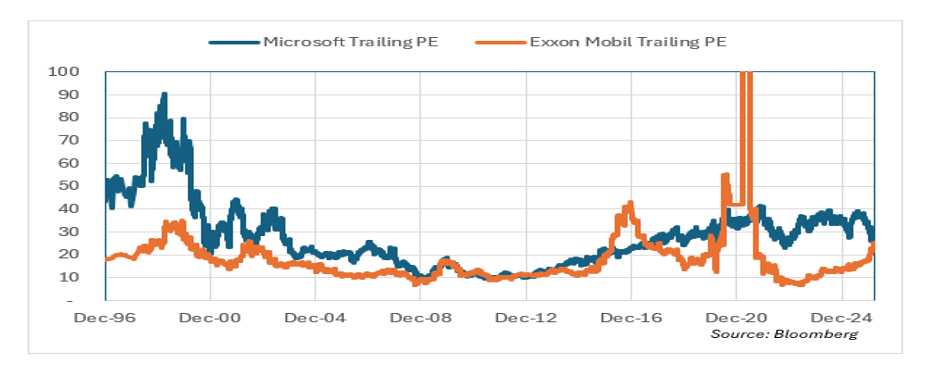

Microsoft now trades at a slightly lower trailing PE multiple than Exxon Mobil. This does not mean that Microsoft stock is a better buy than Exxon Mobil, but it is illustrative of the rapid change in market sentiment.

Mid-Cycle Elections and the Year Ahead

Election years are frequently characterized by heightened uncertainty and uneven market performance. It is common for markets to struggle through the early and middle portions of election years as investors await greater clarity on fiscal policy, regulation, and geopolitical direction.

Historically, markets have often found firmer footing later in election years once the mid-term elections are over. The latter part of the year has frequently delivered stronger returns as clarity improves and economic and market fundamentals reassert themselves.

While near term volatility is likely to persist, especially with the Iran War in the background, Continuity remains focused on long term objectives rather than short term noise. Patience and diversification remain essential. We continue to believe that despite a challenging start, the back half of the year offers the potential for improved equity performance as uncertainty diminishes and markets refocus on fundamentals.