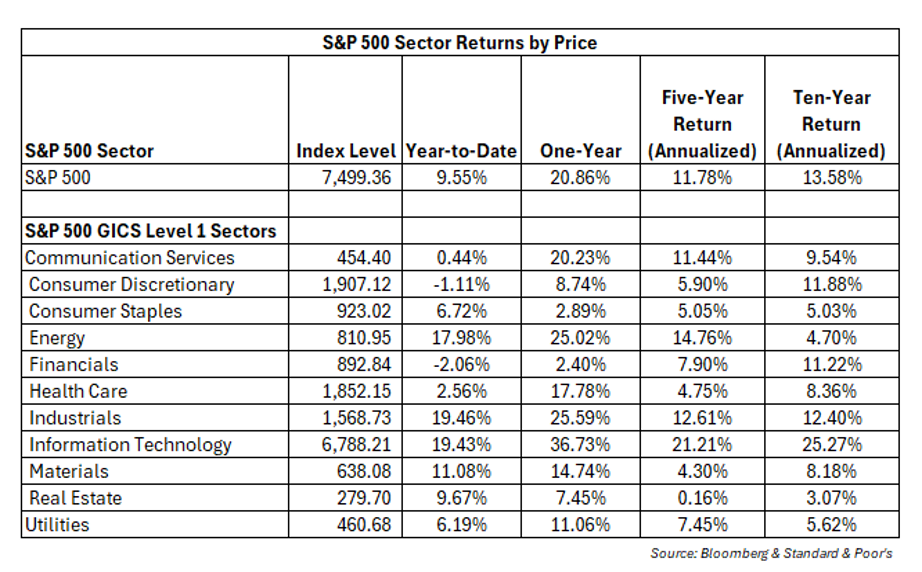

Strong earnings growth and reduced geopolitical risks combined to produce a great quarter for equities. The S&P 500 increased 14.87% in the quarter and is now up 9.55% for the year. The information technology sector, and memory stocks in particular, led the S&P 500 higher.

The S&P 500 information technology sector increased 31.60% in the quarter and is now up 19.43% through the first half of the year. Those numbers were eclipsed by the much-followed Philadelphia Semiconductor Index, which increased 87.75% in the quarter and 101.14% in the first half of the year. This performance was even more impressive given that mega-cap technology stocks lagged.

Oil prices declined 31.45% in the quarter and are now up 21.04% year-to-date. The decline in oil prices on reduced geopolitical risks coincided with energy stock underperformance. The S&P 500 energy sector fell 14.03% in the quarter but is still up 17.98% year-to-date. Industrials, information technology, and energy stocks were the three best sectors in the first half of the year. All three of them increased between 17-20%.

While U.S stocks generated strong returns in the second quarter, the relative returns varied overseas. Developed market stocks performed well, while emerging market stocks roared. The MSCI EAFE Index rose 9.80%, while the MSCI Emerging Markets Index increased 23.31% (Source: Bloomberg).

Emerging market stocks were led by AI capex-related stocks. The three largest weights in the MSCI Emerging Markets Index are the tech stocks Taiwan Semiconductor, Samsung Electronics, and SK Hynix. They comprise about 30% of the Index (Source: MSCI).

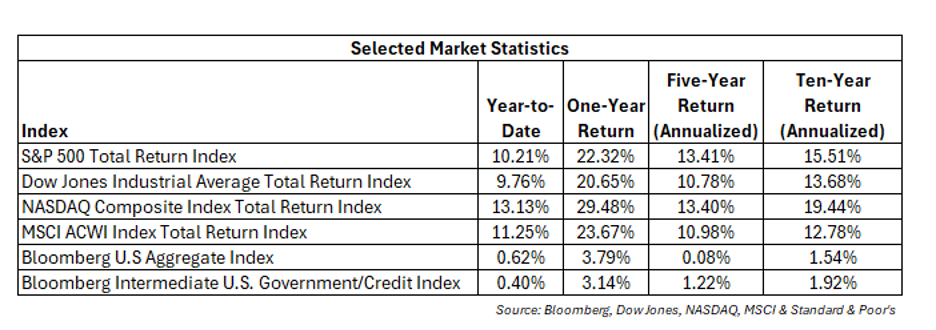

Bonds generated muted returns in the second quarter. The Bloomberg U.S. Aggregate Index increased 0.67% in the quarter while the Bloomberg Intermediate U.S. Government/Credit Index rose 0.43%. Stabilizing bond yields allowed investors to clip coupons in the “safe” portion of their portfolios.

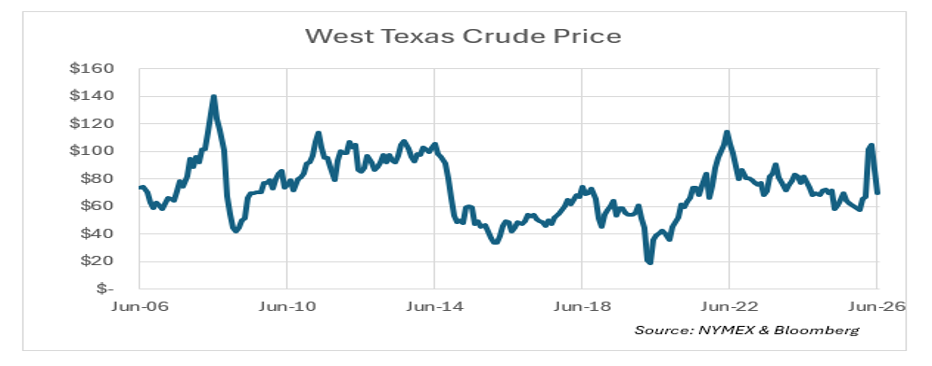

Crude Prices Fall Back to Pre-War Levels

Oil prices spiked at the onset of the Iran War. Prices behaved similarly to 2021-22 at the start of the Ukraine War. The invasion coupled with Iran mining and effectively closing the Strait of Hormuz led to a near doubling in oil prices. An initial price spike was followed by consolidation and then a quick fall in prices back to prewar levels.

On an inflation-adjusted basis, domestic prices are well below their 2008 peak, but that is little comfort to U.S. consumers. West Texas crude prices ended the quarter slightly below the twenty-year average price. The S&P 500 Energy Sector GICS Index has given back more than half of its 2026 gains (Source: Bloomberg). We find it notable that oil prices were unable to maintain a higher price despite the temporary closure of the Strait of Hormuz.

Inflation Inflects Higher

Economy-wide inflation pressures have been building. The inflation rate has been unable to fall back to the Federal Reserve’s stated goal of two percent post-COVID (Source: Bloomberg). Our hope is that an oil price close to seventy dollars a barrel is enough to alleviate some of the inflationary pressures that accelerated due to the war. Unfortunately, we believe that it is unlikely inflation will approach the two percent target any time soon. Continuity thinks lower oil prices are needed to keep inflation below three percent.

Oil prices are not the only reason for the pickup in inflation. The PCE Core Price Index bottomed out in April 2025 and has been trending higher since then (see chart).

Higher oil prices and inflation raise the probability that the Federal Reserve will raise rates. The yield on the Two-Year Treasury Note rose 0.80% since closing February 27th at 3.37% (Source Bloomberg) to end the quarter at 4.17%. Many market participants believe that the Two-Year Treasury leads the Federal Reserve. Accordingly, Fed Funds Futures markets now price in a greater chance of a hike than a cut in 2026, which is a reversal from earlier in the year (Source: Bloomberg).

Rising rates are not conducive to strong fixed income returns. Bond prices move inversely to interest rates unless credit spreads tighten materially. The Bloomberg U.S. Aggregate Index rose a modest 0.62% in the first half of the year after falling 0.05% in the first quarter of 2026. Inflation trends are likely to weigh heavily on moves in interest rates in the second half of the year. Inflation moving convincingly below three percent would probably lead to interest rates coming back down. If that does not happen, a rate hike is likely later this year. Despite the possibility of higher interest rates, we think the outlook for fixed income has improved since the beginning of the year due to rising rates.

Semiconductors Lead, SpaceX Steals Headlines

The S&P 500 ended up 9.55% year-to-date despite falling 4.63% in the first quarter. The reduction in risks due to the Iran War and robust earnings growth helped propel the S&P 500 higher. Despite escalating inflation and elevated geopolitical risks, the market was able to rise. Even with the strong returns, the PE ratio of the S&P 500 barely budged, while the forward PE ratio fell from about 25.6 at the beginning of the year to 21.9 at the end of June (Source: Bloomberg).

Meanwhile, SpaceX made headlines with its initial public offering (“IPO”). Upon its debut, it became the largest U.S. company by market capitalization to go public in history. With a quarter-end market capitalization of $2.2 trillion, there are only five American companies with a higher value. The IPO priced at $135 per share, peaked at $225.64, before closing the quarter at $170.86, for a gain of 26.56% for investors who owned it upon offering (Source: Bloomberg).

Second Half Outlook

This is a mid-term election year, and the returns tend to be subpar in this part of the presidential cycle. That was not the case though in the first half of the year with equity markets experiencing above-average gains. Our team at Continuity suspects that there will be more volatility as we get closer to the November 3rd election.

Markets dislike uncertainty and the path of interest rates is uncertain. Chair Warsh appears to be more hawkish, at least in the short term, than Chair Powell was. Risk has been priced out of the Iran War, but it is not settled yet.

Additionally, the August-to-October period is frequently volatile. From 1990 onward, the S&P 500 has averaged modest gains in July and small drops in August and September (Source: Bloomberg). As such, we would expect the second half of the year to be choppy until the mid-term elections. However, Continuity does not see a reason to turn bearish. Earnings growth remains strong and the economy is showing few signs of a slowdown.